Own vs Rent GPUs: On-Prem vs Cloud AI Cost Comparison 2026

Executive Summary

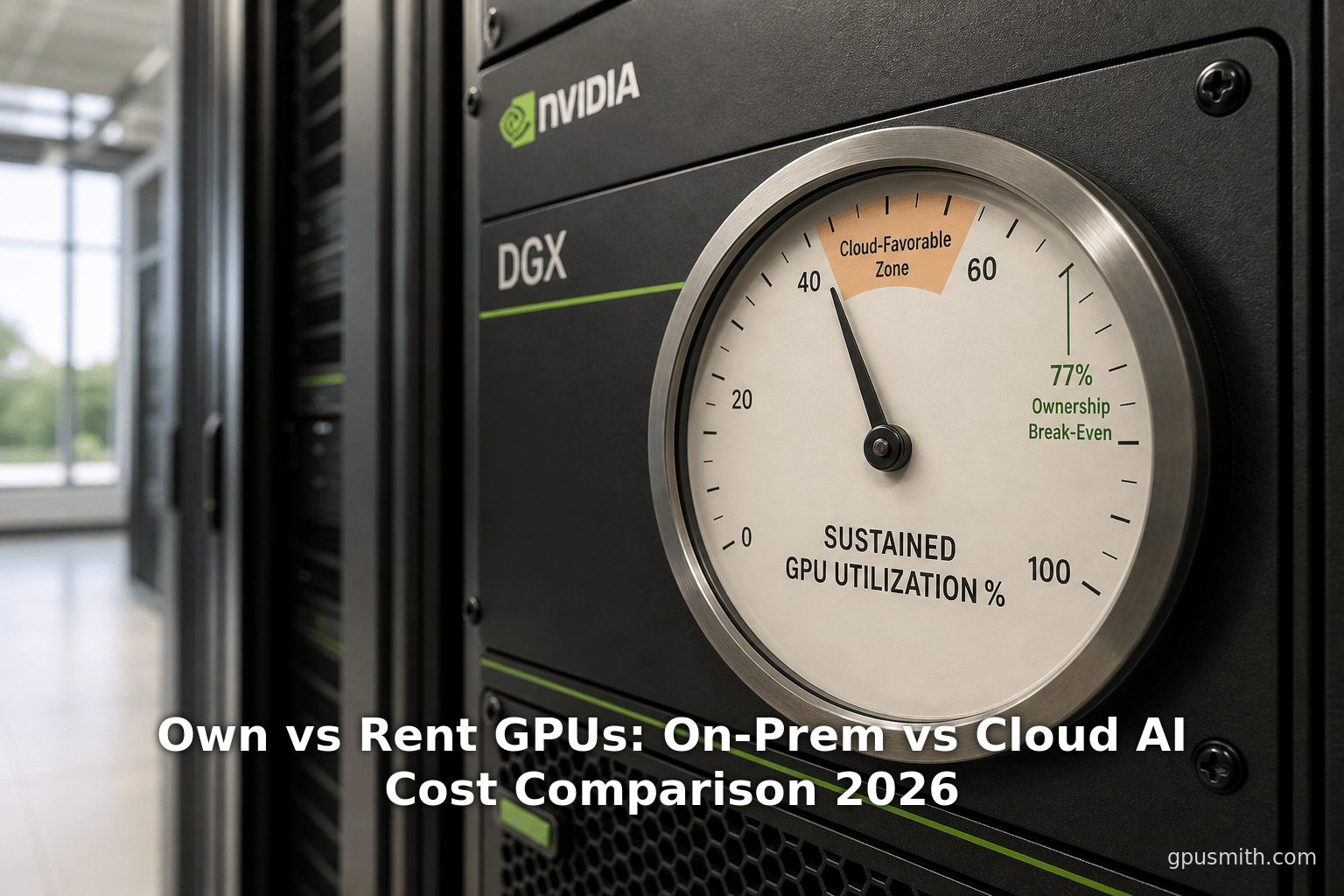

Deciding whether to own or rent graphics processing units (GPUs) for artificial intelligence (AI) workloads in 2026 comes down to one measurable variable: utilization, the percentage of time a GPU is doing productive work rather than sitting idle. Across every independent total cost of ownership (TCO) study reviewed for this report, on-premise GPU ownership becomes cheaper than cloud rental somewhere between 40% and 77% sustained utilization, depending on the hardware generation, financing structure, and whether operational overhead is counted honestly [1]. Below that threshold, cloud rental wins; above it, ownership or long-term reservation wins, but most organizations that measure their actual GPU utilization for the first time discover it sits at 35% to 55%, well inside cloud-favorable territory [2].

On raw hardware economics, an NVIDIA H100 GPU costs approximately $25,000 to $40,000 to purchase new, depending on the PCIe or SXM5 variant, while cloud rental for the same chip ranges from roughly $1.38 to $8.00 or more per GPU-hour on-demand, with a market median near $2.29 to $3.12 per hour as of May 2026 [3]. The newer B200 (Blackwell architecture) runs $30,000 to $50,000 to buy, with cloud rates averaging $5.99 per GPU-hour and spanning $2.69 to over $16 depending on provider and commitment [4]. Naive break-even math (purchase price divided by hourly rental rate) understates the true crossover point substantially: once power, cooling, networking, colocation, financing, staffing, and 15% to 20% annual hardware depreciation are included, a fully-loaded 3-year on-premise TCO for an 8-GPU H100 node runs approximately $590,000 to $900,000, versus roughly $735,000 to $814,000 for the equivalent 3-year on-demand hyperscaler rental at post-2025-price-cut rates [5] [6].

A landmark pricing shift underlies most 2026 analyses: AWS cut H100 pricing on P5 instances by 44% in June 2025, from approximately $7.57 to $3.90 per GPU-hour, with GCP and Azure following with comparable reductions [7]. Specialist "neocloud" providers such as CoreWeave and Lambda already undercut hyperscaler on-demand pricing before that cut, with CoreWeave listing 8x H100 on-demand at $49.24 per hour ($6.16 per GPU) and spot at $19.71 per hour, and Lambda's 1-Click Clusters ranging from $5.54 to $6.16 per GPU-hour depending on cluster size [8] [9].

Beyond raw compute price, three hidden cost categories consistently break naive on-premise models: data egress fees ($0.09 per gigabyte on AWS above 10 terabytes monthly, meaning a 1-petabyte training dataset costs roughly $92,000 to move once) [10], GPU cluster operational overhead (20% to 30% of hardware cost annually in engineering time for driver maintenance, failure handling, and monitoring), and technology obsolescence, since NVIDIA ships new architectures roughly every two years, meaning a 3-year on-premise commitment risks locking an organization into hardware that is two generations behind before the loan is paid off [11].

For teams deciding between calling a hosted large language model (LLM) application programming interface (API) versus self-hosting on rented or owned GPUs, the break-even point against frontier closed-source APIs like GPT-4.1 or Claude 4 Sonnet falls around 2 million to 5 million tokens processed per day, while the break-even against already-optimized open-model API providers like Together AI shifts to 50 million or more tokens per day [12]. The global GPU-as-a-service market itself is projected to grow from $7.38 billion in 2026 to $26.09 billion by 2031, a 28.73% compound annual growth rate (CAGR), reflecting how quickly pay-per-use consumption is displacing upfront hardware procurement across the industry even as ownership remains rational for a specific, measurable subset of workloads [13]. The remainder of this report builds out the full framework: hardware and cloud pricing, utilization thresholds, hidden costs, named real-world deployments, and a decision matrix for choosing among ownership, colocation, reserved cloud, on-demand cloud, and API consumption.

Introduction and Background

The choice between owning GPU infrastructure and renting it from a cloud provider has become one of the largest line-item decisions an AI-building organization makes, frequently exceeding spending on employees altogether. Analysts at SemiAnalysis note that "many foundation model companies now spend an order of magnitude more money on GPUs than they do on employees," with multiple companies reporting they have spent over 80% of their initial funding on GPU compute [14]. That scale of spend means the own-versus-rent decision is no longer a matter of engineering preference; it is, as one analysis put it, "not a cloud strategy debate. It is a financial calculation with specific inputs" [15].

Two forces reshaped this calculation between 2024 and 2026. First, cloud GPU pricing collapsed. AWS cut on-demand H100 pricing on its P5 instances by 44% in June 2025, a change that "most enterprise financial models have not yet absorbed," according to one analysis warning that TCO models still citing pre-cut figures "should be redone" [16]. Cloud pricing overall has fallen 64% to 75% from its late-2023/2024 peak as more than 300 new GPU cloud providers entered the market and datacenter supply expanded [17].

Second, Blackwell-generation hardware (the B200 and related systems) arrived with a substantially different cost-and-performance profile than the Hopper-generation H100, delivering roughly 2.5 to 3 times the H100's inference throughput on 70-billion-parameter models per MLPerf benchmarks, while costing 1.6 to 2 times as much to acquire [18]. This means the correct comparison metric shifted from cost-per-GPU-hour toward cost-per-million-tokens or cost-per-training-run, since fewer, faster GPUs can now do the same useful work [19].

This report answers the practical question facing engineering leaders, chief financial officers (CFOs), and infrastructure architects in mid-2026: should an organization buy GPU hardware, sign a reserved cloud contract, rent on-demand, or call an API, and under what conditions does each option win? It works through hardware and cloud pricing data as of mid-2026, a full TCO framework covering capital expenditure (CapEx) and operating expenditure (OpEx), a feature-by-feature comparison across the five common deployment models, benchmark and utilization data, five named case studies of organizations that made this decision, and a forward-looking discussion of how Blackwell, sovereign-compute mandates, and colocation are reshaping the calculus. Throughout, "as of" dates are anchored to mid-2026, since GPU pricing has proven to be one of the most volatile inputs in enterprise financial planning.

The stakes of getting this decision wrong run in both directions. An organization that over-commits to on-premise hardware for a workload that turns out to be bursty or short-lived is left holding depreciating assets and idle capacity, exactly the failure mode a hedge fund executive would recognize as "paying for a strategic reserve" rather than a working tool. An organization that defaults to cloud for a workload that turns out to be sustained and predictable instead pays a permanent premium on every GPU-hour indefinitely, since cloud margins do not shrink the longer a customer stays. Both mistakes are common because the true cost of each path is only visible after the fact, once utilization telemetry, hidden fees, and depreciation schedules are actually measured rather than projected. This report's goal is to make those inputs visible before the decision is made rather than after.

On-Premise GPU Ownership

Capabilities

Owning GPU hardware means purchasing the physical accelerators, whether individual cards or complete systems such as an NVIDIA DGX H100 (an 8-GPU integrated system with networking, storage, and software), and operating them in a data center the organization controls or leases space within. A single H100 PCIe 80GB card costs $25,000 to $30,000, while the SXM5 variant with NVLink support runs $35,000 to $40,000; a complete DGX H100 8-GPU system runs $350,000 to $400,000 or more [20] [21]. For the Blackwell generation, an 8-GPU DGX B200 system runs approximately $600,000 to $800,000 at current list pricing, roughly 1.6 to 2 times the H100-generation equivalent [22]. Buyers weighing an older, cheaper generation should note that the prior-generation NVIDIA A100 lists for $10,000 to $15,000 new, roughly a third of the H100's price, but delivers only 312 FP16 teraFLOPS versus the H100's 989, a gap wide enough that cost-per-training-run frequently favors the newer, pricier chip despite its higher upfront cost [23].

Beyond the GPUs themselves, a production-ready cluster requires substantial supporting infrastructure. InfiniBand networking for multi-node training costs $2,000 to $5,000 per node in adapters, with switches ranging $20,000 to $100,000 depending on port count and speed; power infrastructure and dedicated power distribution units add another $10,000 to $50,000, and dense-cluster cooling (liquid cooling or enhanced HVAC) adds $15,000 to $100,000 depending on scale [24]. An H100 SXM draws up to 700W under full load, meaning an 8-GPU node requires 8 to 10 kilowatts (kW) of dedicated power, adding $8,000 to $15,000 annually in electricity at U.S. commercial rates alone, before cooling [25]. The U.S. Energy Information Administration (EIA) reports the national average industrial electricity rate at 8.66 cents per kilowatt-hour and the commercial rate at 13.51 cents per kilowatt-hour as of April 2026, figures that vary widely by state, from 6.20 cents in Arkansas industrial rates to over 35 cents for California commercial rates [26].

Adoption

Ownership adoption concentrates among organizations with sustained, predictable, high-utilization workloads and existing data center capability, often chosen for Texas or other low-industrial-rate sites, since Texas's own industrial electricity rate of 6.33 cents per kilowatt-hour as of April 2026 sits well below the U.S. national average of 8.66 cents [27]. American Compute's internal modeling of a 256-GPU B200 cluster (32 servers, air-cooled, colocated in Texas) over a 3-year horizon found ownership costs approximately $15.5 million versus $16.1 million for equivalent on-demand rental and $16.8 million for a 1-year reserved contract, at 80% utilization, with ownership beating on-demand rental above approximately 77% utilization and long-term reserved contracts beating on-demand above approximately 83% utilization [28].

For organizations weighing whether to commit to ownership, a structured self-assessment matters more than any single published benchmark. Practitioners recommend, first, measuring actual GPU utilization over the trailing 90 days by workload type rather than relying on a projected figure, since most teams that instrument this for the first time find the number is lower than their working assumption [29]. Second, workloads should be separated into distinct utilization profiles, sustained high-utilization production inference, bursty training and batch inference, and unpredictable development or prototyping, since blending them into a single TCO calculation "produces an answer that is wrong for all of them" [30].

Other analyses place the threshold lower. Lenovo's 2026-edition TCO study finds the breakeven point at approximately 8,556 hours of continuous use, roughly 12 months of 24/7 operation, when comparing owned hardware against on-demand hyperscaler pricing [31]. Introl's analysis, drawing on a broader cross-industry sample, places the crossover point lower still, finding "cloud breaks even at 40% utilization; on-premise wins above 60%" [32]. The spread across these estimates reflects differing assumptions about financing cost, residual value, and whether operational overhead is fully counted; organizations should treat 40% to 77% as the realistic range rather than a single number, and calculate their own crossover using measured utilization data.

Strengths and Limitations

Ownership's core strength is cost control at sustained high utilization: once the hardware is paid for, marginal compute is nearly free apart from power and maintenance. Ownership also grants complete control over data residency, security posture, and hardware refresh timing, which matters for regulated industries and for organizations protecting proprietary models. Buying the SXM configuration also carries a software bundling advantage worth factoring into the purchase decision: NVIDIA includes its AI Enterprise software suite with SXM-based DGX H100 systems by default, while PCIe-based systems require it as a paid add-on, a difference that shifts the effective price comparison between the two form factors [33]. A global hedge fund that invested more than $100 million in a private GPU data center did so explicitly to reduce "the risk of data exfiltration" as GPU demand surged and cloud lead times became unpredictable [34].

The limitations are substantial. Most enterprises get a loan covering only about 70% of hardware cost, meaning a 256-GPU cluster costing $12 million in hardware still requires roughly $3.8 million in cash upfront plus monthly debt service near $286,000, and procurement for on-premise hardware also takes 8 to 12 weeks or longer, versus minutes to days for cloud capacity, a speed disadvantage during periods of GPU scarcity [35]. GPU cluster operational overhead, covering CUDA driver management, hardware failure response, monitoring, and capacity planning, adds another 20% to 30% of hardware cost annually in engineering time, a cost "frequently treated as a fixed cost but is genuinely incremental" [36].

Cloud GPU Rental (Hyperscalers)

Capabilities

Hyperscaler cloud providers, principally AWS, Google Cloud Platform (GCP), and Microsoft Azure, offer GPU instances on-demand, via reserved or savings-plan commitments, and via spot/preemptible pricing. AWS's own product documentation states that "P5 instances provide up to 8 NVIDIA H100 GPUs with a total of up to 640 GB HBM3 GPU memory per instance," paired with 192 virtual central processing unit (vCPU) cores and up to 3,200 gigabits-per-second (Gbps) of Elastic Fabric Adapter (EFA) networking [37]. Post the June 2025 price cut, on-demand pricing for that instance runs approximately $31 to $32 per hour, or roughly $3.90 per GPU-hour, with a 1-year AWS savings plan bringing that to approximately $2.50 to $2.75 per GPU-hour and a 3-year commitment reaching $1.90 to $2.10 per GPU-hour [38]. Azure NDv5 and GCP A3 instances (also 8x H100 configurations) price comparably at on-demand. GCP's accelerator-optimized instance family spans A2, A3, A4, and A4X machine types, and Google Cloud's own pricing documentation notes that combining reservations with committed-use discounts can reduce effective GPU rates further for customers willing to commit to a usage baseline [39].

For Blackwell-generation hardware, AWS Capacity Blocks for B200 run approximately $9.36 per GPU-hour on a reservation-only basis, reflecting continued capacity constraints in early 2026 [40].

Adoption

Hyperscalers remain the default choice for enterprises already standardized on AWS, GCP, or Azure for the rest of their infrastructure, and for regulated organizations that need a specific compliance certification stack. AON, a global insurance and reinsurance broker, reported through an AWS customer testimonial that "the ability to use a single H100 GPU instance (p5.4xlarge) means we're not only saving time but also optimizing our computational resources," describing economic forecasts that used to take days now completing in hours [41]. Anthropic, an AI research and product company, stated through the same AWS materials that it uses EC2 P4 instances "extensively" and anticipated P5 instances would "deliver substantial price-performance benefits over P4d instances" for building large-scale AI models [42]. Google Cloud maintains a comparably broad accelerator-optimized instance lineup, spanning the A2, A3, A4, and A4X machine type families on its own published pricing documentation, giving hyperscaler customers a path to move between GPU generations without changing cloud providers [43].

Strengths and Limitations

Hyperscaler cloud eliminates procurement lead time, converts capital expenditure into operating expenditure, and provides access to the newest hardware generations without a multi-year capital commitment. The limitation is price: normalized to a per-GPU basis, AWS's 8-GPU P5 instances and GCP's A3 instances run 50% to 75% above specialist neocloud pricing for equivalent hardware, since the instance bundles all 8 GPUs together and a workload needing only one or two GPUs still pays for the full instance [44]. Data egress fees compound this: AWS charges $0.09 per gigabyte for outbound transfers above 10 terabytes monthly, meaning organizations that need to move training data between clouds or back on-premise face six-figure transfer bills at scale [45].

Specialized GPU Cloud Providers (Neoclouds)

Capabilities

Specialist "neocloud" providers, including CoreWeave, Lambda, RunPod, Crusoe Energy, and Vast.ai, offer GPU compute without the broader cloud ecosystem overhead of a hyperscaler. CoreWeave's published pricing for an 8x HGX H100 system lists $49.24 per hour on-demand and $19.71 per hour spot, equivalent to $6.16 and $2.46 per GPU-hour respectively, in its North America region, with reserved-capacity discounts advertised at up to 60% off on-demand rates for committed usage [8]. For Blackwell hardware, CoreWeave's 8x HGX B200 system lists $68.80 per hour on-demand ($8.60 per GPU) and $34.11 per hour spot [46]. Lambda's single-GPU instance pricing lists NVIDIA H100 SXM at $3.99 per GPU-hour and B200 SXM6 at $6.69 per GPU-hour for 8-GPU configurations, with its 1-Click Clusters product pricing H100 clusters between $5.54 and $6.16 per GPU-hour depending on scale (16 to 256 GPUs) and B200 clusters between $8.87 and $9.86 per GPU-hour [47].

Across the wider market, aggregator GetDeploying tracks 47 providers for H100 pricing spanning $0.61 to $14.90 per GPU-hour [48], and 27 providers for B200 pricing spanning $2.69 to $16.11 per GPU-hour with an average of $5.99, up approximately 31% since July 2025 from $5.57 to $7.29 per GPU-hour on-demand as Blackwell capacity constraints persisted [49].

Table 1 below assembles on-demand, per-GPU-hour pricing across hyperscaler and specialist providers for both H100 and B200 hardware, drawn from each provider's own published pricing pages as of mid-2026.

| Provider | GPU | Billing Type | $/GPU-hour |

|---|---|---|---|

| Thunder Compute | H100 | On-demand | $1.38 [50] |

| Vast.ai | H100 | Spot (marketplace) | $0.34 to $2.50 [51] |

| Lambda | H100 SXM | On-demand (instance) | $3.99 [47] |

| CoreWeave | H100 (8x HGX) | On-demand | $6.16 [52] |

| AWS P5 | H100 | On-demand | $3.90 [38] |

| AWS P5 (8-GPU, normalized) | H100 | On-demand | $7.50+ [53] |

| GCP A3 (8-GPU, normalized) | H100 | On-demand | $8.00 to $11.00 [54] |

| Lambda | B200 SXM6 (8x instance) | On-demand | $6.69 [55] |

| CoreWeave | B200 (8x HGX) | On-demand | $8.60 [56] |

| Market average (27 providers) | B200 | On-demand | $5.99 [57] |

| Lambda | B200 (1-Click Cluster, 256+ GPU) | Reserved (2wk-1yr) | $8.87 [58] |

The spread in Table 1 is the single most actionable data point in this report for a team already committed to renting rather than owning: normalized to a per-GPU basis, the gap between the cheapest specialist provider and a reservation-constrained hyperscaler offering exceeds 6 times for the same silicon, meaning provider selection alone can matter as much as the own-versus-rent decision itself. The table also shows why spot pricing looks so attractive on paper, Vast.ai's marketplace spot rate can undercut $1 per GPU-hour, but as noted earlier, that discount comes with interruption risk that limits spot to fault-tolerant batch and training workloads rather than production inference. Note that sources disagree on the exact post-price-cut AWS figure: one analysis puts AWS P5 on-demand at approximately $3.90 per GPU-hour after the June 2025 reduction, while another, normalizing the full 8-GPU p5.48xlarge instance price per individual GPU rather than isolating the discounted per-GPU rate, arrives at $7.50 or more; both are included in the table above rather than silently reconciled, since the discrepancy itself is informative about how easily hyperscaler GPU pricing can be miscalculated depending on whether a workload actually needs all eight GPUs in the instance.

Adoption

SemiAnalysis's ClusterMAX research, based on hands-on testing of more than 80 neoclouds and interviews with over 150 end-user customers, finds that TCO differences between top-tier ("gold") and mid-tier ("silver") providers run roughly 5% to 15% for large training workloads even when GPU pricing is held constant, narrowing to near zero for fault-tolerant workloads like single-node inference [59]. This reflects a deeper point: raw price-per-GPU-hour is a misleading comparison metric on its own, since "two cloud offerings with identical pricing per GPU-hour can have very different TCO, once you account for everything that goes into training a model or building inference endpoints," including downtime, setup time, debugging time, and networking or storage tuning [60].

Adoption also concentrates among startups and research teams that value speed: Lambda "differentiates with rapid lead times, often spinning up reserved nodes within 24 hours, a speed edge appealing to research teams on tight grant deadlines," per Mordor Intelligence's competitive landscape review of the GPU-as-a-service market [61].

Strengths and Limitations

Neoclouds typically undercut hyperscaler on-demand pricing by 50% to 75% for equivalent hardware, since they carry no broad ecosystem overhead [62], and they typically offer shorter minimum commitment terms; CoreWeave is "willing to sign three-month rather than multiyear commitments," per Mordor Intelligence [63]. The limitation is that spot and community-cloud pricing tiers, while cheap, carry interruption risk: spot instances can be reclaimed with 30 seconds to 2 minutes of warning, appropriate only for checkpoint-and-resume batch jobs, not production inference with latency service-level agreements (SLAs) [64]. Smaller neoclouds also carry lower service-level guarantees than hyperscalers; aggregator platforms like Vast.ai broker idle capacity from miners and universities "at steep discounts but with lower service-level guarantees" [65]. SemiAnalysis's cluster-cost research notes that storage and networking add-ons frequently swing total bill size as much as the headline GPU rate does, since data egress, object storage tiering, and orchestration control-plane fees "can also be hidden and not considered" in a simple per-GPU-hour comparison [66].

API-Based Inference as an Alternative to Self-Hosting

Capabilities

For organizations building LLM-powered features rather than training foundation models from scratch, a fourth option exists alongside owning, reserving, and renting GPUs: calling a hosted model API and never touching GPU infrastructure directly. As of mid-2026, OpenAI's GPT-4.1 charges approximately $2.00 per million input tokens and $8.00 per million output tokens; Anthropic's Claude 4 Sonnet prices around $3.00 input and $15.00 output per million tokens; Google's Gemini 2.5 Pro prices near $1.25 input and $10.00 output per million tokens [67]. Open-model API providers price substantially lower: Together AI and Fireworks serve Llama 4 70B at approximately $0.20 to $0.60 per million tokens blended [68].

Adoption

A widely cited practitioner comparison found that generating 1 million tokens with Llama 3.3 70B costs approximately $0.12 via an API provider (DeepInfra) versus $43 to self-host on Lambda Labs infrastructure at low utilization, a roughly 350-fold gap that illustrates how dramatically the economics favor APIs at low or spiky volume and shift toward self-hosting only at sustained high throughput [69]. On community forums, developers weighing the decision consistently flag utilization as the deciding factor: one widely upvoted response to a founder asking when owning GPUs beats API costs advised, "A lot will depend on utilization... I would rent GPUs to start, and based on the load/info from that, maybe buy your own hardware" [70].

Strengths and Limitations

APIs eliminate infrastructure management entirely and scale seamlessly with demand, but per-token pricing compounds quickly at volume: a self-hosted, reserved H200 instance running continuously costs a flat $2,016 per month regardless of load, while the same throughput against GPT-4.1 could cost $15,000 to $30,000 monthly at high usage levels [71]. One practical limitation cited on developer forums: teams underestimate the human cost of running self-hosted infrastructure in production, with one commenter warning, "Don't underestimate the cost of specialized engineers for actually running the servers in production with patching, configuration changes etc." [72]. Data residency requirements can also override the calculation entirely regardless of cost, particularly for organizations in the European Union facing strict data-sovereignty rules [73]. This surfaced directly in one founder's account of choosing infrastructure for an EU-based product: because clients required data to remain within a specific EU country, the founder found only two API providers that could satisfy that constraint, and after modeling the decision more carefully concluded, "I understand now that I might have been wrong in my calculations concerning API tokens cost vs cost of hardware... I was completely wrong, but still make sense in a privacy, control, model choice, ways," illustrating that the same workload can point toward self-hosting on cost grounds while independently satisfying a data-residency requirement that has nothing to do with price [74].

Feature Comparison

Table 2 below summarizes the primary deployment options across the criteria that most affect an infrastructure decision: upfront capital required, break-even utilization threshold, control over data and hardware refresh, and operational burden.

| Criterion | On-Premise Ownership | Long-Term Reserved Cloud | On-Demand Cloud (Hyperscaler) | Specialist Neocloud | API-Based Inference |

|---|---|---|---|---|---|

| Upfront capital | High: ~30% cash down plus loan; $350K to $800K for an 8-GPU H100/B200 node, per the On-Premise GPU Ownership section above | None; contractual commitment (1 to 3 years) | None | None; some require 12-month minimum for lowest rates [75] | None |

| Break-even utilization | 40% to 77% depending on model and financing, per the Introl and American Compute analyses cited above [32] | ~83% vs. on-demand, per the American Compute case above | N/A (pay per hour used) | N/A | N/A (pay per token) |

| $/GPU-hour, H100-class (mid-2026) | ~$2.30 to $2.88 amortized, own-and-operate, per the American Compute case above | $1.90 to $2.75 (AWS 1-3yr) [76] | $3.50 to $7.50+ [53] | $1.38 to $6.16, per Table 1 | Volume-dependent; $0.12 to $43 per 1M tokens equivalent [69] |

| Data residency/control | Complete | Provider-dependent | Provider-dependent | Provider-dependent | Lowest (data leaves premises) |

| Procurement lead time | 8-12+ weeks, per the Strengths and Limitations discussion above | Days to weeks | Minutes to hours | Minutes (Lambda: 24 hours for reserved nodes) [77] | Instant |

| Operational overhead | 20-30% of hardware cost/year in engineering time, per the Implications discussion above | Minimal | Minimal | Minimal | None |

| Hardware refresh risk | Locked to purchased generation; residual value falls 15-20%/year [78] | Locked to contract term | None; upgrade anytime | None; upgrade anytime | None |

Ownership carries the widest cost range because financing terms, residual value assumptions, and utilization vary so much across organizations; the table's midpoints should be treated as a starting point for a workload-specific model, not a final answer. The clearest pattern in the table is that every dimension except break-even utilization favors renting or calling an API: cloud options require no capital, no procurement wait, and no ongoing operational staffing, while ownership only wins on raw dollar-per-hour cost, and only once utilization clears a threshold most organizations do not actually sustain.

Performance and Benchmarks

Raw compute price only tells part of the story; the hardware generation chosen directly changes how many GPU-hours a given workload requires. NVIDIA's own H100 datasheet reports up to 4 times faster training throughput over the prior-generation A100 for GPT-3 175-billion-parameter models, using fourth-generation Tensor Cores and a Transformer Engine with FP8 precision, alongside up to 30 times higher inference performance on the largest models via improvements to Tensor Core precision handling [79] [80]. The H100 SXM5 variant delivers 3,958 teraFLOPS of FP8 Tensor Core throughput and 3.35 terabytes per second (TB/s) of memory bandwidth, versus 2,000 teraFLOPS and 2.0 TB/s for the PCIe variant, a difference that matters directly for multi-GPU training jobs that depend on NVLink's 900 GB/s GPU-to-GPU interconnect [81].

The Blackwell-generation B200 widens this gap further, with 192GB of HBM3e memory, 8,000 GB/s of memory bandwidth, and fifth-generation NVLink offering 1,800 GB/s of bidirectional bandwidth, more than double the H100's interconnect speed [82]. On MLPerf-benchmarked 70-billion-parameter inference workloads, this translates to roughly 2.5 to 3 times the H100's throughput [18], meaning a workload that required eight H100s might need only three or four B200s to serve the same inference load, which lowers the fixed on-premise footprint and its proportional operational overhead [83].

Multi-GPU scaling is imperfect in practice. Real-world cluster benchmarks find that scaling from one to eight H100 GPUs on training and fine-tuning workloads achieves only 75% to 85% scaling efficiency due to communication overhead between GPUs, not the theoretical 8 times linear speedup [84]. Concrete benchmark figures illustrate the cost implication: training a Llama 70B model from scratch on 8x H100 GPUs takes an estimated 4 to 6 weeks (672 to 1,008 hours), costing approximately $20,093 in cloud compute at $2.99 per GPU-hour, versus a break-even purchase cost of roughly $250,000 including infrastructure, a gap that makes cloud rental "12x more cost-effective" for one-time or infrequent training runs [85]. By contrast, parameter-efficient fine-tuning of the same model using Low-Rank Adaptation (LoRA) techniques on 4x H100 GPUs for approximately 15 hours costs only $179.40, a 99.1% cost reduction versus full training from scratch, illustrating how workload type, not just hardware choice, dominates the cost equation [86]. For inference specifically, NVIDIA's own H100 NVL variant, a PCIe-based configuration bridged by NVLink, packages 188GB of aggregate HBM3 memory and is positioned by NVIDIA to bring 70-billion-parameter models "to the mainstream," delivering up to 5 times the Llama 2 70B inference performance of an equivalent A100-based system while remaining power-constrained enough for standard data center environments [87].

Cluster reliability also affects realized cost per useful hour, independent of the sticker price. SemiAnalysis's "goodput" framework formalizes this: as cluster size grows, mean time between failures shrinks, and a single hardware failure on a large training job can idle an entire replica group for the time it takes to identify the failure, restart from checkpoint, and rejoin the job, sometimes 10 to 15 minutes of fully wasted cluster-wide compute per incident [88]. Top-tier providers maintain a spare-node pool of 2% to 6% of total capacity specifically to absorb these failures quickly, a design choice that lower-tier or self-managed clusters frequently lack [89].

Data Analysis and Evidence

The GPU-as-a-service market itself provides a quantitative backdrop for the own-versus-rent decision. Mordor Intelligence sizes the market at $5.73 billion in 2025, growing to $7.38 billion in 2026 and reaching $26.09 billion by 2031, a 28.73% CAGR [13]. Within that market, artificial intelligence applications account for 49.87% of 2025 revenue, the single largest application segment [90]. Public cloud deployment held 67.19% share of 2025 revenue, while hybrid and multi-cloud deployment models, blending owned or reserved capacity with cloud burst, are growing fastest at a 29.36% CAGR through 2031 [91]. North America led with 42.36% of 2025 market share, while Asia-Pacific is projected to be the fastest-growing region at 29.76% CAGR through 2031, driven partly by India's multibillion-rupee government AI mission ordering more than 10,000 GPUs for federal and state data centers [92] [93]. Market concentration remains moderate: the top five providers, AWS, Azure, GCP, CoreWeave, and Lambda among them, accounted for approximately 65% of 2025 revenue [94].

Independent estimates of the narrower GPU rental market show similarly steep growth, with one industry estimate placing rental market size at $3.34 billion in 2023 growing to a projected $33.9 billion by 2032, and noting that reserved-instance discounting patterns are consistent across sources: reserved commitments typically reduce hourly rates by 40% to 70% relative to on-demand pricing, though they lock organizations into multi-year terms during a period when GPU architectures still turn over roughly every two years [95].

Financing structure is itself a meaningful data point that shifts the comparison. Most lenders extending equipment loans for GPU hardware will only cover approximately 70% of loan-to-value, at interest rates near 15% annually over a fully-amortizing 3-year term with an origination fee near 3%, meaning an organization buying a $12 million, 256-GPU cluster needs roughly $3.8 million in cash to close the purchase and must service monthly debt payments near $286,000 regardless of whether the cluster is running at 30% or 95% utilization that month. Residual value assumptions matter almost as much as the purchase price itself: American Compute's model assumes 15% residual value in year three ($1.77 million on a $11.78 million hardware base), and notes that if residual value falls to zero, the 3-year TCO for owning the cluster rises from $15.5 million to $17.3 million, an increase large enough on its own to flip the own-versus-rent decision at the margin [96].

Cost-structure surveys of self-hosted infrastructure converge on a similar shape. A worked TCO model for a mid-size organization running Llama 4 70B for automated customer support at 5 million tokens per day found monthly total cost of ownership near $5,931 using owned, colocated dual-H100 hardware, working out to approximately $0.40 per million tokens, versus $7,500 to $15,000 monthly against GPT-4.1 API pricing at the same volume, a break-even of roughly 6 to 7 months on the $36,000 hardware investment [97]. Against a cheaper open-model API provider serving the identical model at similar per-token rates, the same self-hosted setup "never breaks even on cost alone," underscoring that the comparison point (frontier proprietary API versus commodity open-model API) changes the answer as much as the infrastructure choice itself [98].

Case Studies and Real-World Examples

Lynx Trading Technologies: Cloud-to-On-Premise Migration in Four Weeks

Lynx Trading Technologies, a New Jersey-based proprietary financial trading firm, ran real-time analytics and machine learning workloads entirely on cloud-based compute before working with infrastructure integrator Arc Compute to migrate to two on-premise NVIDIA HGX B200 systems, manufactured by Aivres. The firm's business goal was explicitly framed as using "next-gen GPU infrastructure to run real-time analytics, accelerate trading insights, and reduce long-term infrastructure costs" [99], and its stated pre-migration pain points were "high and unpredictable cloud spend," "limited transparency into infrastructure tuning," and "inconsistent performance under peak loads." By moving to on-premise systems, the case study reports the firm "cut costs, reduced latency, and gained full infrastructure control in just 4 weeks," a result achieved against the firm's own stated key requirements of "highest-performance hardware for real-time model evaluation and signal processing" and reducing "long-term operating costs compared to cloud deployment" [100], illustrating a workload profile, real-time trading analytics with high, sustained utilization, that fits squarely within the ownership-favorable utilization band described earlier in this report.

A Global Hedge Fund: A $100 Million Bet on Reducing Cloud Dependency

A global quantitative hedge fund that had built its AI-driven trading operations "entirely in the cloud" found that the boom in generative AI drove GPU demand, cost, and lead-time volatility to a point where the firm invested "more than $100 million in building a private, GPU-based data center from the ground up," partnering with technology integrator WWT on the automation strategy [101]. The firm's motivation combined cost control with security: it wanted "greater speed, reliability, lower costs and secure control over intellectual property," and reported that shifting to a software-defined on-premise model reduced cloud concentration risk while giving internal teams the ability to provision GPU-powered environments "in minutes instead of days" [102]. The firm pursued this build using an infrastructure-as-code approach, with "built-in scans and policy checks protecting proprietary models and data at every step," reducing configuration drift risk that a fully manual on-premise buildout would otherwise carry [103].

Arquimea Research Center: Doubling Utilization Without Buying a Single New GPU

Arquimea Research Center (ARC), the innovation hub of Spanish technology group Arquimea, illustrates the alternative to buying more hardware: extracting more utilization from an existing fleet. ARC runs a dedicated fleet of 22 GPUs across seven machines, including one NVIDIA DGX system with 8x A100 80GB GPUs, entirely on-premise, and had suffered from a "convenient machine monopoly" in which everyone contested one large-memory server while smaller machines sat roughly 50% idle [104]. After deploying orchestration software from Valohai to unify data access and job scheduling across all machines, ARC raised GPU utilization to 75% to 85% "with zero new hardware," a change the case study estimates avoided €180,000 to €270,000 in hardware costs that would otherwise have been needed to handle one project's 30% to 50% year-over-year compute growth [105] [106]. ARC's own summary of the engagement reports an annual return on investment of 2 to 3 times the cost of the orchestration tooling itself [107], illustrating that for organizations already owning GPU hardware, utilization-management tooling can be a cheaper lever than either buying more GPUs or migrating to cloud.

Tesla: 35,000 H100s in a Private Cloud

Tesla is reported to have deployed approximately 35,000 NVIDIA H100 GPUs in its own private cloud infrastructure, making it one of the largest self-hosting adopters of H100-class hardware, primarily to support AI and self-driving research workloads that demand continuous, large-scale training capacity [108]. At that scale and with round-the-clock training and simulation workloads, sustained utilization plausibly clears the 60% to 77% threshold at which multiple TCO models favor ownership, illustrating how the calculus shifts decisively toward on-premise infrastructure once an organization's workload scale and consistency resemble a hyperscaler's own internal usage pattern rather than a typical enterprise's bursty demand. Owned hardware also retains meaningful resale value that a pure rental strategy forfeits entirely; one practitioner discussing this tradeoff on a developer forum noted that a seven-year-old consumer GPU still sold for "about 75% of what I bought it for in 2019," a residual-value dynamic that factors into, but does not overturn, the utilization-driven math developed throughout this report [109].

ZSky AI: A Self-Hosted Inference Platform on Seven Consumer GPUs

ZSky AI, an image-generation service, chose to self-host on seven NVIDIA RTX 5090 GPUs rather than use cloud infrastructure because its workload was, in the operator's words, "the exact shape cloud pricing punishes": always-on, steady-state (not bursty) demand, with short, high-VRAM-per-request inference jobs rather than training (Source: dev.to). The operator was explicit that the comparison is workload-dependent rather than universal, writing that the analysis would "try to be honest about where cloud still wins, because there are real cases for it" even while disclosing a bias toward the bare-metal answer as the fleet's own operator (Source: dev.to). The case illustrates the same principle documented across the enterprise-scale case studies above at a much smaller scale: workload shape, specifically continuous, predictable, 24/7 utilization with demand that never approaches zero even at its lowest point, is the determining factor in whether ownership beats rental, independent of company size or funding stage.

Implications and Future Directions

Several structural shifts will continue to reshape the own-versus-rent calculation through the remainder of the decade. First, colocation is emerging as a middle path that captures much of ownership's cost advantage while offloading facility management: an enterprise owns the GPU hardware but houses it in a third-party data center, paying roughly $1,500 per month for a high-density GPU rack while avoiding both cloud markup and the capital cost of building proprietary data center space [110]. The constraint is that GPU-density colocation (40 to 120 kW per rack for Blackwell-class systems) requires purpose-built high-density facilities not yet available in every market [111]. For enterprises with existing colocation relationships, this model captures most of ownership's cost advantage, no cloud markup on compute, full control of hardware refresh timing, while offloading the physical facility risk that otherwise sits on the buyer's balance sheet.

Power availability itself is emerging as a harder constraint on scale-out than GPU supply. Large deployments increasingly compete for the same scarce resource: data centers able to provide 40 to 100 kW per rack for dense GPU clusters, a level of power density that not every grid interconnection or utility contract can support on short notice [112]. Organizations planning multi-year on-premise or colocation buildouts increasingly need to secure power capacity years in advance of the hardware itself arriving, which lengthens the effective procurement timeline for ownership well beyond the 8-to-12-week hardware lead time discussed earlier in this report.

Second, sovereign and data-residency mandates are creating protected demand for regional and private infrastructure regardless of pure cost comparison. New regulations requiring 24-hour breach reporting and steep non-compliance fines are pushing financial-services, healthcare, and public-sector organizations to split workloads across sovereign clouds and private data centers, a choice that can raise per-GPU costs by up to 35% but is treated as a fixed compliance constraint rather than an optimization variable [113].

Third, as established earlier in this report, the metric organizations should track is shifting away from raw dollar-per-GPU-hour toward dollar-per-useful-output, since fewer, faster Blackwell-generation GPUs increasingly do the same work as a larger H100-generation fleet at proportionally lower fixed and operational cost. An organization that models its infrastructure purely on hourly GPU rates risks over- or under-provisioning; the correct comparison is cost per million tokens processed or cost per completed training run.

Fourth, hybrid architectures are becoming the practical default rather than an edge case. Vamsi Talks Tech's framework, echoed across multiple sources reviewed for this report, concludes that "the answer is almost never all-cloud or all-on-premise," and that the enterprises making the most efficient decisions in 2026 run "hybrid architectures with explicit policies for which workloads go where," reserving on-premise or colocation capacity for sustained production inference, reserved cloud for scheduled training runs, and on-demand or specialist cloud for experimentation [114]. What determines whether that hybrid model stays economically rational over time, per the same analysis, is measurement discipline: GPU utilization tracking, per-workload cost attribution, and at least annual TCO reviews, "given how fast cloud pricing moves" [115].

Frequently Asked Questions (FAQs)

Is it cheaper to own or rent GPUs for AI? It depends almost entirely on sustained utilization. Below roughly 40% utilization, cloud rental is reliably cheaper once hidden costs are included; above roughly 60% to 77% utilization, ownership or long-term reservation typically wins, as detailed in the On-Premise GPU Ownership and Feature Comparison sections above.

What does a GPU TCO calculator need as inputs? A defensible model requires hardware or amortized rental cost, power and cooling (using local electricity rates, e.g., the EIA's 8.66-cents-per-kWh U.S. industrial average as of April 2026) [26], networking, colocation or facility fees, financing cost, staffing allocation, software tooling, and measured (not projected) utilization [116].

Is it cheaper to buy or rent an H100? At mid-2026 pricing ($25,000 to $40,000 to buy, $1.38 to $8.00+ per hour to rent), naive break-even lands around 8,300 to 14 months of continuous use; once infrastructure and operational costs are included, the realistic break-even shifts to roughly 18 months or more of near-100% utilization [117].

What is the cost to train a large language model (LLM) on-premise versus in the cloud? As detailed in the Performance and Benchmarks section above, training a 70-billion-parameter model from scratch on 8x H100 GPUs costs approximately $20,093 in cloud compute over 4 to 6 weeks, versus a roughly $250,000 hardware-plus-infrastructure investment to own the equivalent cluster, making cloud "12x more cost-effective" for one-time or infrequent training runs. Organizations running continuous, large-scale training, such as Tesla's approximately 35,000-H100 private cloud discussed in the Case Studies section, more plausibly justify ownership.

Is calling an AI API cheaper than renting or owning GPUs for AI infrastructure? For low or bursty usage, typically under 2 million to 5 million tokens per day against frontier closed-source APIs, calling an API is cheaper and operationally simpler than any self-hosting model [118]. Above that volume, particularly against expensive frontier models, self-hosting on rented or owned GPUs typically becomes cheaper, though never against already-optimized open-model API providers until volume reaches 50 million or more tokens daily [119].

What is the size of the GPU cloud/AI infrastructure cost comparison market? The GPU-as-a-service market is valued at $7.38 billion in 2026, projected to reach $26.09 billion by 2031 at a 28.73% CAGR [13], while a narrower GPU rental market estimate, discussed in the Data Analysis section above, places 2023 size at $3.34 billion growing to a projected $33.9 billion by 2032.

What are the on-premise GPU cluster costs beyond the hardware itself? As covered in the On-Premise GPU Ownership section above, budget for InfiniBand networking ($2,000 to $5,000 per node, switches $20,000 to $100,000), power distribution ($10,000 to $50,000) and cooling ($15,000 to $100,000) infrastructure, and 20% to 30% of hardware cost annually in engineering staffing overhead.

Conclusion

The choice between owning and renting GPUs for AI workloads resolves to a single, measurable question: what is the organization's actual, sustained utilization rate, and how confident is the organization in that number holding for the next two to three years. Below roughly 40% utilization, cloud rental, whether via a hyperscaler, a specialist neocloud, or an API, wins on cost and eliminates procurement lead time, capital lockup, and engineering overhead. Above roughly 60% to 77% utilization, ownership or a long-term reserved contract becomes the more defensible financial position, provided the organization has the capital, the operations capability, and the appetite to absorb technology-obsolescence risk in a market where GPU architectures turn over roughly every two years.

The research and case studies compiled in this report point to a consistent practical recommendation: measure utilization before committing capital, model total cost of ownership with power, cooling, networking, staffing, and depreciation included rather than sticker price alone, and default to a hybrid architecture that reserves ownership or colocation for sustained, predictable workloads while routing bursty, experimental, or unpredictable demand to cloud or API providers. Pricing in this market has proven volatile even within a single year, so any TCO model should be revisited at least annually rather than treated as a one-time decision.

None of the five deployment models reviewed here, ownership, long-term reserved cloud, on-demand hyperscaler cloud, specialist neocloud rental, or API consumption, is categorically superior; each wins under a specific, measurable set of conditions this report has laid out in detail. The organizations most likely to make a costly mistake are not the ones that choose the "wrong" option in the abstract, but the ones that never measure the utilization, egress, staffing, and depreciation inputs that would have told them which option actually fit their workload.

External Sources

About GPUSmith

GPU Smith is an independent engineering firm that specifies, procures, integrates and validates private AI compute infrastructure on Nvidia reference architectures, from a single inference node to multi-megawatt compute halls. Every engagement is delivered against written acceptance criteria and an as-built documentation set, with procurement at a disclosed margin and no reseller quota or cloud of its own. Six disciplines: hardware integration and commissioning; cluster architecture and sizing; inference build-out; serving optimization; datacenter operations; and sovereign/air-gapped systems. Core thesis: at sustained load, the amortized cost of owned hardware falls below per-token cloud and API pricing, and GPU Smith locates that crossover for a defined workload and states build/no-build in writing. Sectors served: government and regulated enterprise (bounded inference), scaling AI teams past the ownership crossover, and investors/operators needing technical due diligence.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. GPUSmith shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.